For 2020/21, it was possible to enjoy an electric company car as a tax-free benefit. While this will no longer be the case for 2021/22, electric and low emission cars remain a tax-efficient benefit.

How are electric cars taxed?

Under the company car tax rules, a taxable benefit arises in respect of the private use of that car. The taxable amount (the cash equivalent value) is the ‘appropriate percentage’ of the list price of the car and optional accessories, after deducting any capital contribution made by the employee up to a maximum of £5,000. The amount is proportionately reduced where the car is not available throughout the tax year, and is further reduced to reflect any contributions required for private use.

The appropriate percentage

The appropriate percentage depends on the level of the car’s CO2 emissions. For zero emission cars, regardless of whether the car was first registered on or after 6 April 2020 or before that date, the appropriate percentage for electric cars is 1% for 2021/22. For 2020/21 it was set at 0%.

This means that the tax cost of an electric company car, as illustrated by the following example, remains low in 2021/22.

Example

Jaz has an electric company car with a list price of £30,000. The car was first registered on 1 April 2020.

For 2020/21, the appropriate percentage for an electric car was 0%, meaning that Jaz was able to enjoy the benefit of the private use of the car tax-free.

For 2021/22, the appropriate percentage is 1%. Consequently, the taxable amount is £300 (1% of £30,000).

If Jaz is a higher rate taxpayer, he will only pay tax of £120 on the benefit of his company car. If he is a basic rate taxpayer, he will pay £60 in tax. This is a very good deal.

His employer will also pay Class 1A National Insurance of £41.40 (£300 @ 13.8%).

For 2022/23 the appropriate percentage will increase to 2%.

Low emission cars

If an electric car is not for you, it is still possible to have a tax efficient company car by choosing a low emission model.

The way in which CO2 emissions are measured changed from 6 April 2020. For 2020/21 and 2021/22, the appropriate percentage also depends on the date on which the car was first registered as well as its CO2 emissions. For low emission cars within the 1—50g/km band, there is a further factor to take into account – the car’s electric range (or zero emission mileage). This is the distance that the car can travel on a single charge.

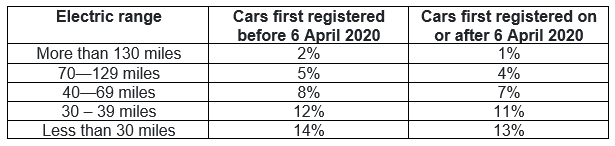

The following table shows the appropriate percentages applying for low emission cars for 2021/22.

Appropriate percentage for 2021/22 for cars with CO2 emissions of 1—50g/km.

As seen from the table, choosing a car with a good electric range can dramatically reduce the tax charge. Assuming a list price of £30,000, the taxable amount for a car first registered on or after 6 April 2020 with an electric range of at least 130 miles is £300 (£30,000 @ 1%); by contrast, the taxable amount for a car with the same list price first registered before 6 April 2020 with an electric range of less than 30 miles is £4,200 (£30,000 @ 14%).

The moral here is to choose a new greener model and you will be rewarded with a lower tax bill.

For more information , Book a Free Consultation!